Mortgage lending has never been a low-stakes industry. But the compliance pressure lenders are dealing with right now, like layered federal rules, aggressive state-level legislation, and a CFPB that can pivot its enforcement priorities mid-year, has made the back-office reality genuinely difficult to manage.

Most lenders aren’t struggling because they don’t understand the regulations. They struggle because the operational side can’t keep up. Documents need to go out fast, teams are stretched, and the systems holding everything together were often built for a simpler time.

That’s the actual problem. And it’s why the conversation around compliance automation, specifically around CCM platforms, matters more now than it did even a few years ago.

The Regulatory Environment Isn’t Getting Simpler

Let’s be direct about the landscape you’re operating in.

Regulatory change is hitting mortgage lending from multiple directions at once, the CFPB’s enforcement priorities, Fannie Mae’s updated cybersecurity requirements, and a growing body of state-level rules that don’t always align with each other. A lender operating in five states is effectively managing five separate compliance programs, each with its own documentation requirements, disclosure language, and submission deadlines.

The cost of getting it wrong is documented and public. The FDIC cited 65 HMDA violations in 2024 alone, most stemming from data collection errors, not intentional misconduct; just the predictable result of manual processes running at scale without proper controls in place.

These aren’t obscure technical failures. They’re the predictable result of scaling a manual process past its breaking point. Which means the fix isn’t more training, it’s better systems.

![]()

Evaluate document automation tools with confidence and reduce compliance risks.

Download the guide to compare vendors and make smarter decisions fast.

What Most Lenders Get Wrong About “Compliance Automation”

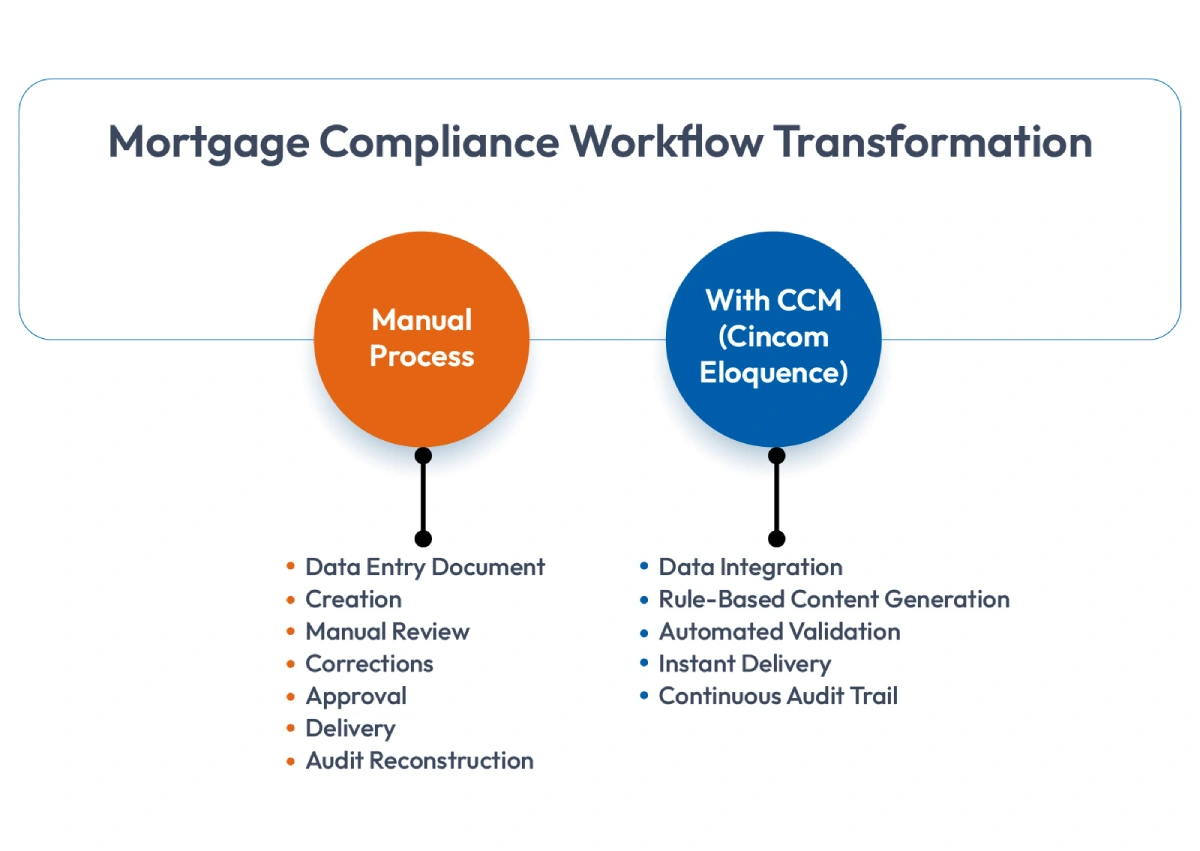

This comes up in almost every conversation with lenders evaluating whether they actually need a CCM platform. The answer is usually some version of: we already have automation built into our workflow.

And in most cases, that’s true, but the automation stops at document generation. A system that creates a disclosure faster isn’t the same as a system that ensures the disclosure is correct. Speed without control just means you can produce a non-compliant document more efficiently.

Real compliance automation does something structurally different. It builds the rules into the creation process itself, so what comes out the other end is already validated, not waiting to be reviewed afterward.

That distinction, between checking after and enforcing during, is what actually changes the risk profile for a lending organization. It’s also what most lenders discover they’re missing when something goes wrong.

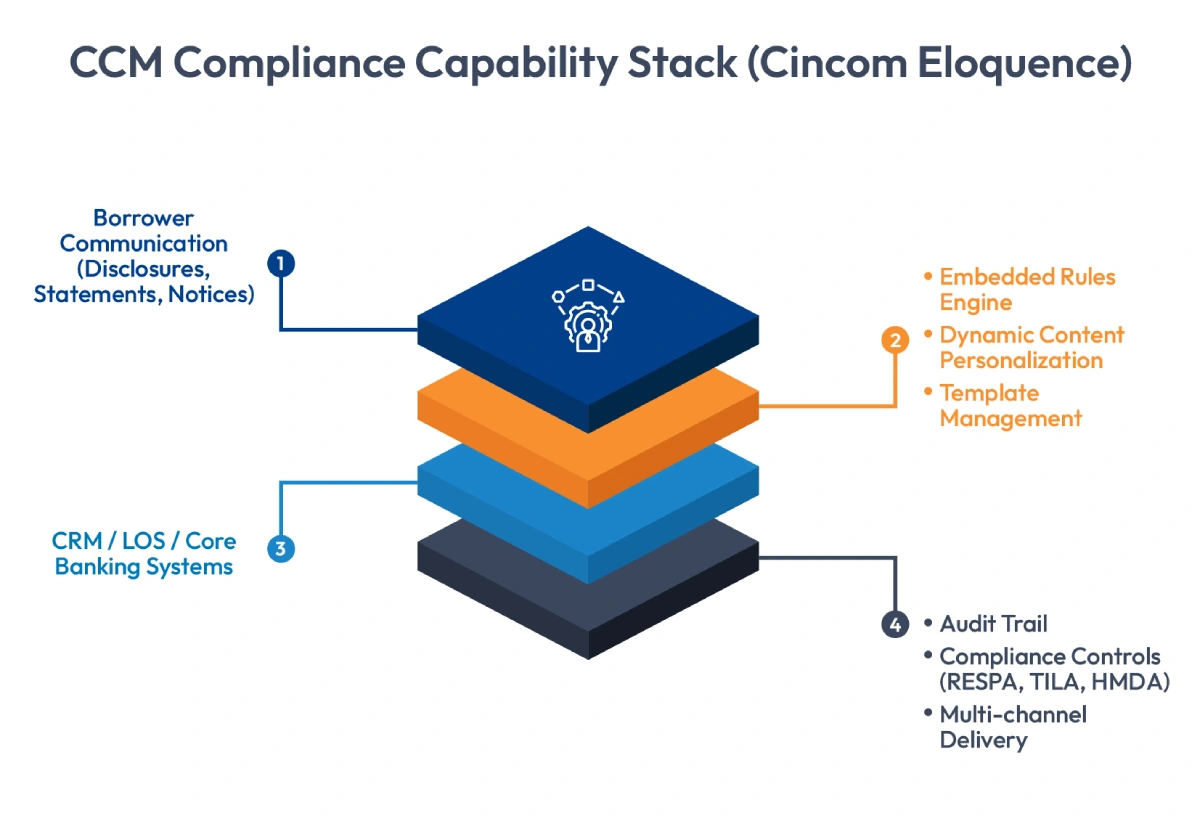

Where Cincom Eloquence Fits into the Compliance Picture

A CCM platform isn’t just a document tool. Done right, it functions as a control layer that sits across your entire outbound borrower communication operation, from the first loan estimate and disclosures through closing documents and post-closing servicing notices.

Cincom Eloquence is built specifically for this kind of financial services complexity. Here’s what that means in practice for mortgage lenders:

Embedded rules logic for error-free content: Rather than relying on staff to know what goes into which document under which conditions, Eloquence encodes those rules directly into the communication workflow. The right content, disclosures, and language are pulled automatically based on loan type, borrower profile, jurisdiction, and other variables. The output is compliant by design, not by luck or by whoever happened to review it that day.

Centralized template management: When your disclosure templates live in multiple locations across different departments, updates don’t propagate evenly. One team works with a current version; another doesn’t know it changed. Eloquence brings everything into a single source solution, where changes happen once and apply everywhere immediately. That alone closes a significant compliance gap.

Real-time and batch document generation on one platform: Mortgage operations don’t run on a single rhythm. Some documents need to go out in bulk at end of day; others need to be generated immediately at the point of application. Eloquence handles both on the same platform, without requiring separate systems or separate workflows.

Audit-ready record keeping: Regulators don’t just want compliant communications; they want proof. Who received what, when, in which version, through which channel. Reconstructing that manually during an examination is time-consuming and error-prone. Eloquence maintains that record continuously, automatically, so when the question comes up, the answer is already there.

Easy integration with existing infrastructure: One of the more practical concerns lenders have is whether a new platform will play well with what they already have. Eloquence’s Service-Oriented Architecture (SOA) is designed for seamless integration with existing core systems, without heavy IT involvement for ongoing updates and changes.

The Borrower Experience Piece That Usually Gets Left Out

Here’s something that doesn’t come up often enough in compliance conversations: the quality of borrower communication is itself a compliance issue, not a separate customer experience metric.

According to the JD Power 2025 U.S. Mortgage Servicer Satisfaction Study, just 32% of customers give their mortgage servicers a high overall communication rating.

That’s a low number in any industry. In mortgage lending, where the timing, clarity, and completeness of borrower communications carry legal weight under TILA, RESPA, and ECOA, it’s a number that should make compliance officers genuinely uncomfortable.

A disclosure that’s technically present but practically incomprehensible isn’t a strong regulatory shield. A servicing notice that goes through the wrong channel, or with stale account information, creates both a borrower’s experience failure and potential regulatory exposure. These aren’t separate problems; they’re the same problem showing up in two different places.

Eloquence’s dynamic content generation and real-time digital sensing allow financial institutions to tailor communications to each customer’s preferences, account type, and situation. The result is communication that’s both more compliant and more useful to the person receiving it.

What to Actually Look for When Evaluating CCM Platforms

Not everything that calls itself a CCM platform is built for the compliance demands of mortgage lending. A few things worth probing specifically:

Does it have embedded rules logic, or just basic conditional logic? Basic conditional logic like “if loan type A, use template B” is table stakes. A genuine rules engine handles multi-variable conditions simultaneously: loan type, borrower profile, state jurisdiction, regulatory version, communication channel. Mortgage compliance requires the latter.

How does it handle multi-state regulatory variation? This is where many platforms fall short. What’s required in one state isn’t necessarily what’s required in another. The system should manage that variation automatically, not through manual workarounds for each individual loan file.

Can business users make template changes without IT involvement? If every regulatory update requires a developer to touch the system, your response time to compliance changes will always lag behind the regulatory timeline. Cincom Eloquence is specifically built so customer-facing teams can update content and communication rules with minimal IT support, a practical difference that matters when a rule changes mid-quarter.

What does the audit trail actually look like? Ask to see it. Some platforms log delivery confirmations and nothing else much. What you need is version history, data inputs, the channel used, timestamps, and confirmation of receipt, the full picture that regulators will expect.

Is it a single source solution or a patchwork? Managing batch and interactive document generation across separate platforms creates synchronization gaps and version control problems. A single platform for all communication types eliminates that category of risk entirely.

What Implementation Actually Looks Like

Choosing the right platform is step one. Getting the implementation right is a different challenge, and it’s where a lot of the value gets left on the table.

The most common mistake is treating the CCM platform like a document generation tool and not configuring the rules engine with enough care. The platform enforces the rules you give it. If compliance expertise doesn’t inform the configuration, if the people who understand RESPA, TILA, and state-level disclosure requirements aren’t involved in how the rules are set up, the system will generate documents quickly, but not necessarily correctly.

Deferring core system integration is another one. Budget pressures make this tempting. But running manual data transfers “temporarily” has a way of becoming permanent, and that’s exactly the gap where data errors enter the process and HMDA violations start accumulating.

Then there’s template governance. The whole value of a single source solution depends on actually keeping it centralized. The moment individual teams start maintaining their own versions, even with good intentions, the model starts to erode.

The Honest Case for Acting Now

According to research, the Customer Communication Management (CCM) market size is expected to exceed USD 6100 million by 2034, with a CAGR of 9.9%, reflecting increasing demand for personalized and digital customer interactions. Financial services are the largest vertical by revenue share, which reflects one straightforward reality: manual communication management at scale doesn’t work in a complex regulatory environment, and the industry knows it.

The lenders handling compliance well aren’t necessarily the ones with the largest compliance teams. They’re the ones who’ve made compliance structural, built into how documents are created and communications are sent, rather than managed as a separate review layer on top of everything else.

As Brent Hochstetler, IT Application Services Manager at Everence, put it after implementing Cincom Eloquence: “Cincom showed a willingness to learn our business and explained how their Eloquence solution could be easily integrated with our existing infrastructure and applications to yield significant improvements in the speed of template development, testing and approval to generate error-free, personalized document communications.”

That’s what the shift looks like in practice, not a rip-and-replace, but a structured integration that makes the compliance work faster, more controlled, and easier to demonstrate when it matters most.

![]()

See how Everence improved document management and reduced costs with Cincom Eloquence.

Download the case study to explore the results.

Questions Worth Asking Before You Commit to a Platform

- At what point in the workflow does data move from your core systems into the CCM platform and is any of that manual?

- How are multi-state regulatory differences handled: automatically, or through manual configuration per loan?

- If a regulation changes mid-quarter, how quickly can the relevant templates and rules be updated, and by whom?

- What does the examination-ready audit trail look like. Can you see a live example?

- Can the platform handle both high-volume batch runs and real-time individual document generation on the same system?

The answers will tell you quickly whether a platform is built for the operational reality of mortgage compliance or just built to look like it is.

If you want to know whether Cincom Eloquence can provide answers to these questions, talk to an expert!

FAQs

1. Which regulations does Cincom Eloquence support for mortgage and financial services compliance?

Eloquence is built to support regulatory compliance across financial services broadly, including AML, KYC, GDPR, FATCA, and MiFID II, with audit trails, version control, and standardized communication workflows. For US mortgage operations, the platform’s embedded rules logic and document governance capabilities directly support RESPA, TILA, ECOA, and HMDA compliance requirements.

2. How long does implementation typically take?

For a mid-sized financial institution, a phased rollout with proper core system integration and compliance rules configuration typically runs three to six months. Rushing it tends to produce a system that’s fast but not actually controlled, particularly around rules configuration and template migration.

3. Can business users manage template changes without IT support?

Yes, this is one of Eloquence’s core design principles. Customer-facing teams can update templates, apply conditional logic, and manage communication content with minimal IT involvement. That matters a lot when regulatory changes require a fast turnaround.

4. What’s the practical difference between Cincom Eloquence and a document management system?

A document management system organizes and stores what’s already been created. Eloquence controls what gets created in the first place, the rules, the content, the data inputs, the delivery channel, and the audit record. The compliance value lives in that control layer, not in storage.

5. How does Eloquence help during a regulatory examination?

Rather than manually reconstructing what was sent and when, Eloquence maintains a continuous, detailed audit trail, version used, data included, delivery method, timestamp, and confirmation. Examination prep that used to take weeks can happen in hours.