What Are CFPB Compliance Communication Requirements?

The Consumer Financial Protection Bureau (CFPB) communication requirements are a set of federal rules that govern how banks must interact with their customers across the entire relationship. We are talking about loan disclosures, account statements, collection notices, error resolution letters, adverse action notices, and more. Every one of these has rules around content, timing, delivery channel, and recordkeeping.

What makes this challenging is the scope. Any bank, credit union, or mortgage servicer under CFPB supervision has to follow multiple rules consistently, at scale, across every channel. Getting the notice out is only half the job. You also need to prove you sent the right version to the right person, at the right time, when an examiner asks.

The Key CFPB Regulations Banks Must Follow

In the CFPB compliance communication, there is no single rule. There is a stack of them, and each one targets a different part of the customer relationship. Missing any one of them during an exam is not a small oversight; it becomes a pattern finding.

Let’s walk through each one.

Regulation X: Mortgage Servicing

This one carries the heaviest communication burden. If a borrower misses a payment, specific timelines trigger immediately. A written early intervention notice must be sent by the 45th day of delinquency. Additionally, loss mitigation updates follow strict schedules, and force-placed insurance requires multiple written notices before the first charge is applied.

Regulation B: Adverse Action Notices (ECOA)

When a bank denies credit, the customer has a right to know why, specifically. A written notice must go out within 30 days, and the reasons must be precise. Vague language has been a consistent exam finding for years; the reason must be actionable rather than general.

![]()

Regulators are not looking for explanations. They are looking for records.

The 2026 Banking Communication Compliance Handbook shows you exactly how to build communication controls that hold up when it matters most.

Regulation F: Debt Collection Communications

Once a bank makes first contact with a borrower about a debt, a validation notice must follow within 5 days. There is also a hard cap of 7 calls per week per debt. Documentation of every contact attempt is mandatory.

Regulation Z: Loan Disclosures (TILA/TRID)

Regulation Z under TRID produces two distinct notice obligations at two different points in the mortgage process. The “Loan Estimate” must go out within 3 business days of the application. The “Closing Disclosure” must reach the borrower at least 3 business days before closing. These are separate documents with separate deadlines and separate retention periods. Certain changes during the closing process, including a shift in APR beyond the applicable tolerance, a change in loan product, or the addition of a prepayment penalty, require a corrected closing disclosure and restart the 3-day waiting period from the beginning.

Regulation E: Electronic Transactions and Disputes

When a customer flags an error on an electronic transfer, the bank has 10 business days to investigate and send written findings. If you missed that window, then you will be looking at a strict liability finding, not a judgment call.

Regulation DD: Deposit Account Disclosures

Fee disclosures, interest rates, and account terms all of it needs to be clearly stated upfront. Periodic statements must also include aggregate totals of overdraft and returned item fees, not just transaction-level detail.

UDAAP: The Catch-All Rule

This one sits above all the others. Any communication that misleads a customer, buries critical information, or creates a false impression can trigger a UDAAP finding, even if every other regulation was technically followed.

Quick Reference: CFPB Communication Requirements at a Glance

| Regulation | Communication Type | Key Timing Rule |

| Regulation X | Early intervention notice | By day 45 of delinquency |

| Regulation B | Adverse action notice | Within 30 days of decision |

| Regulation F | Debt validation notice | Within 5 days of first contact |

| Regulation Z (TRID) | Loan Estimate | Within 3 business days of application |

| Regulation Z (TRID) | Closing Disclosure | 3 business days before closing |

| Regulation E | Error resolution notice | Within 10 business days of investigation |

| Regulation DD | Periodic statement | Monthly or quarterly |

| UDAAP | All customer communications | Ongoing |

The Real Cost of Non-Compliance

Non-compliance with CFPB communication requirements carries consequences that go well beyond a regulatory slap on the wrist. Banks that get this wrong may face a combination of financial, operational, and reputational damage that can take years to recover from.

Civil Money Penalties

The CFPB has authority to impose civil penalties ranging from thousands to millions of dollars. The more critical factor is duration. A communication failure that affected customers over several years attracts exponentially higher penalties than a one-time error, and the CFPB has shown it will go back as far as the evidence allows.

Consumer Redress Orders

Banks can be ordered to directly compensate affected customers. When a communication failure touches a large customer base over an extended period, redress orders can climb into the hundreds of millions. Bank of America was ordered to pay $250 million in a 2023 action that included misleading communications around credit card products.

Mandatory Third-Party Audits

Consent orders frequently require independent auditors to review communication practices. This is disruptive and expensive, but the deeper issue is that it hands visibility of your internal processes to an outside party before your team has had the chance to fix them on your own terms.

Board-Level and Personal Liability

Communication failures do not stay confined to the compliance department. Senior executives have faced personal liability in cases where systemic failures pointed to governance breakdowns at the top. In the Fay Servicing case in 2024, the consent order included novel provisions targeting the CEO directly.

State AG Actions and Private Litigation

Many compliance officers focus entirely on federal exposure and underestimate what comes next. State attorneys general hold concurrent authority to act on the same violations. Private litigation under FDCPA, TILA, RESPA, and EFTA moves completely independent of CFPB priorities, meaning even during periods of reduced federal enforcement, your legal exposure does not shrink.

What the regulations and their consequences reveal together is something most compliance officers already sense. The real risk in bank communications does not live in the rulebook; it lives in the daily operational reality of delivering the right notice to the right customer, through the right channel, with full documentation across thousands of touchpoints every single day. That distance between what the policy says and what the process actually delivers is where most banks find themselves exposed, and as the next section shows, the gaps tend to follow a familiar pattern.

Common Communication Compliance Gaps Banks Still Make

Stale Electronic Consent

Banks collect electronic consent at account opening and do not always have a process in place to verify if it is still valid when a critical notice needs to go out. A customer who opted for electronic delivery years ago may have since changed their preferences or stopped accessing their online portal altogether. When a required notice goes out to someone whose consent status has not been recently confirmed, that delivery may not hold up during an exam.

Deadline Tracking Through Manual Processes

Some banks are still managing notice timelines through spreadsheets and calendar reminders. Across a large and growing customer base, this becomes a serious liability because regulatory deadlines do not accommodate staffing gaps, system outages, or simple human error. If a required notice slips through because someone forgot to update a tracker, that explanation carries no weight with an examiner.

Outdated Templates Still Running in Production

When regulations change, legal updates the approved template. What does not always follow is a thorough sweep of every channel and system where that template lives. The updated version gets loaded into the document management system while the old version quietly continues running inside the mortgage servicing platform, the collections queue, and the customer portal. That inconsistency raises both a content accuracy issue and a UDAAP flag that is difficult to walk back once it is on the record.

Adverse Action Notices That Lack Specificity

Regulation B requires denial reasons specific enough to give the customer a genuine understanding of what drove the decision. What examiners frequently encounter are notices that list broad categories like insufficient income or limited credit history without enough detail to be actionable or meaningful to the person receiving them. This has become a growing issue as more banks rely on automated underwriting, because the system can generate a denial without producing language that meets the regulatory specificity standard.

No Record of What Was Actually Sent

A bank may have sent every required notice on time and in the correct format, but without a proper archived record showing what was sent, to whom, through which channel, and under which approved template version, demonstrating compliance during an examination becomes very difficult. The notices may have gone out. If the evidence were not preserved, that distinction would make all the difference.

Missing Translated Communications

The CFPB has flagged language access in mortgage servicing as a recurring area of concern. When loss mitigation communications reach borrowers only in English despite those customers having indicated a preference for another language, it creates both a compliance exposure and a UDAAP risk. Examiners have flagged this pattern consistently, and it is not limited to any one language or region.

These gaps are not unique to any one type of bank. They show up in community banks, regional banks, and large institutions alike because they are process problems, and process problems do not discriminate by size. Addressing them requires more than policy updates and staff training. It requires the right operational infrastructure underneath.

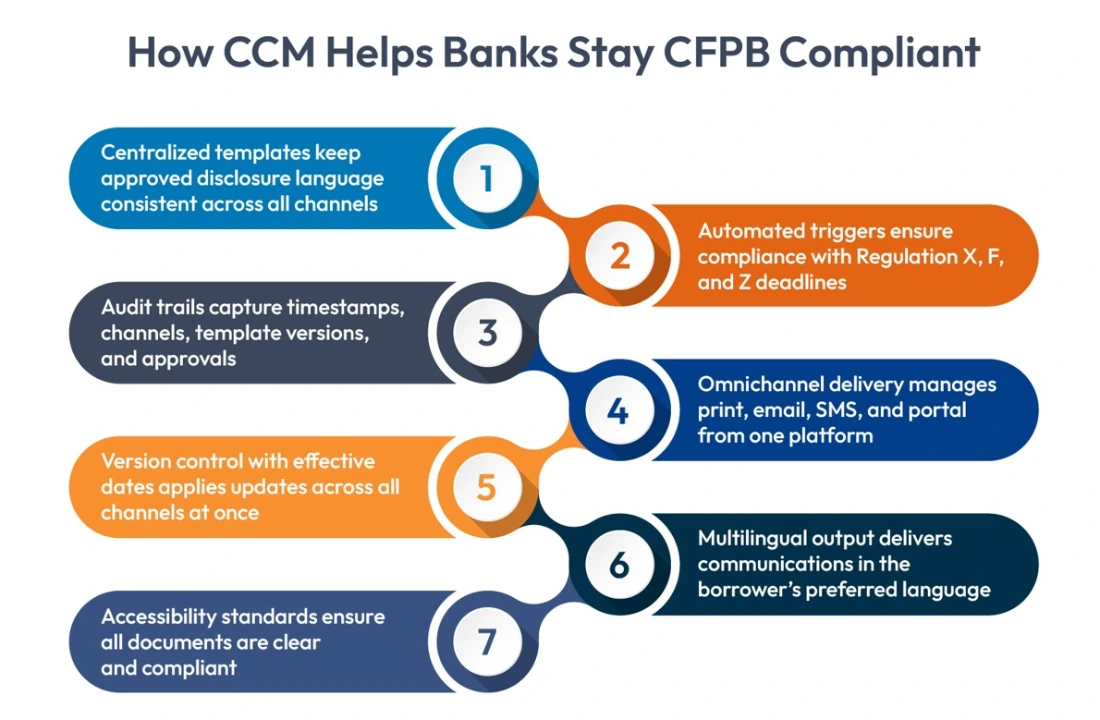

The Role of CCM in Helping Banks Meet CFPB Requirements

Customer Communications Management, commonly known as CCM, is a software category that helps organizations create, manage, deliver, and archive customer communications across every channel. For banks, it sits at the intersection of operations and compliance, giving teams the infrastructure to meet regulatory communication demands consistently and at scale.

The connection between CCM and CFPB compliance is straightforward. Every gap covered in the previous section, whether it is a missed deadline, an outdated template, or a missing audit trail, points to a process that CCM is specifically built to address.

The CCM Capabilities That Actually Matter for Banking Compliance

The CCM market has grown significantly, and there are a lot of vendors making similar claims. When you move past the feature list and into an actual evaluation, these are the areas that separate a solution built for regulated banking environments from one that was adapted for it after the fact.

Implementation Experience in Regulated Environments

A vendor that has never deployed inside a bank’s technology infrastructure will underestimate the complexity of integrating with core banking, loan origination, and servicing systems. Ask for specific financial services deployments, not general enterprise references.

Integration Depth

Surface-level integration that requires manual data exports to trigger notices is not sufficient for a compliance use case. The connection between your core systems and the CCM platform needs to be real-time and event-driven.

Support Model During Regulatory Changes

When regulation changes and templates need to be updated across every channel before a deadline, how does the CCM platform support that process? This is a question worth asking directly and pressing for a specific answer.

Security and Data Governance

Customer communication data is sensitive. The vendor’s security posture, data residency practices, and audit controls should align with your institution’s own compliance and risk standards.

Deployment Flexibility

A solution that only works in one deployment model may not fit your institution’s infrastructure. Cloud, on-premises, and hybrid options matter depending on your bank’s existing architecture.

At the end of the evaluation process, the question worth asking is straightforward. Can this vendor demonstrate, with evidence, that their platform has been held up under the operational and regulatory demands your bank faces every day? If the answer requires qualification, keep looking.

Moving Forward

Building a defensible communication compliance program is less about knowing the regulations and more about having the operational infrastructure to meet them consistently.

If you are doing an honest internal assessment, start by asking where your biggest exposure actually sits. Pull out the last three notice types that required manual tracking and ask how confident you are in the documentation behind them. Look at your template inventory and identify how many versions of the same notice are currently active across different systems. Check whether your electronic consent records are current or whether they reflect the status of your customers at account opening years ago.

These are not comfortable questions, but they are the ones that surface real risk before an examiner does.

The banks that are ahead of this problem have stopped treating communication compliance as a documentation exercise and started treating it as an operational discipline. That shift in thinking is what drives the decision to invest in the right infrastructure, and CCM is where that infrastructure lives for most institutions managing communications at scale.

If you are evaluating CCM solutions for your bank, Cincom Eloquence is built for exactly this kind of operational compliance challenge. It brings together template control, automated triggers, full audit trails, omnichannel delivery, and accessibility conformance in a single platform designed for regulated environments.

![]()

Ready to build a more defensible communication compliance program?

See how Cincom Eloquence helps banks manage regulatory communications at scale.

FAQs

1. How do small and mid-size banks manage CFPB compliance communication without large compliance teams?

Most small and mid-size banks rely on automated CCM platforms to compensate for limited compliance headcount. The platform handles notice generation, deadline tracking, and documentation so the compliance team focuses on oversight rather than execution.

2. What is the first step a bank should take to audit its current CFPB communication program?

Start with your highest risk notice types, mortgage servicing and adverse action notices, and verify that your current process produces a retrievable audit trail for each one. If it cannot, that is where the exposure sits.

3. How does a CCM platform differ from a bank’s existing document management system for bank CFPB requirements?

A document management system stores files. A CCM platform governs the entire communication lifecycle, from template approval and notice generation to delivery, consent tracking, and archival. For bank CFPB requirements, the end-to-end control is what makes the difference in an exam.

4. Can a single CCM platform handle all the different notice types required under CFPB requirements?

Yes, provided the platform supports conditional logic, omnichannel delivery, and integration with core banking systems. A well-configured CCM platform can manage Regulation X, B, F, Z, E, and DD notice types from a single production environment.

5. What is the biggest operational risk banks face when managing CFPB compliance communication manually?

The inability to prove what was sent. Manual processes can generate the right notice but leave no indexed, retrievable record of delivery. In a supervisory review, that evidentiary gap carries the same weight as not sending the notice at all.