Introduction

Customer churn in financial services runs deeper than product dissatisfaction. Forrester’s 2025 CX Index data shows that companies with strong customer experience grow revenue 1.5 to 2 times faster than their competitors, and in financial services, that experience lives or dies in the communication layer.

Most institutions already have multiple communication channels, whether that is the app, the branch, the call center, SMS alerts, or email notifications, but a unified layer connecting them all is where the gap lies, and customers feel that disconnect at every touchpoint.

We recently covered how wealth firms are navigating this shift in The Next-Gen Reconciliation: How Wealth Firms Can Meet Rising Client Expectations with Omnichannel Communication. This piece goes further, breaking down omnichannel vs. multichannel communication for financial institutions, what each model actually means, why regulators are now paying attention to which model you are running, and where most firms stall in making the move.

Multichannel vs Omnichannel: The Difference That Defines Customer Experience

What is Multichannel Communication?

Multichannel communication means your financial institution is present across multiple touchpoints, whether that is a mobile app, a branch, a call center, SMS alerts, or printed statements. Each one operates in its own world, with its own data and its own templates. However, the issue arises because there is no awareness of what happened elsewhere, as all these channels operate in a siloed environment. Consequently, a customer who called support yesterday and opened your app today will have to restart their interaction again, which indicates that your customers are reachable, but they are not connected.

What is Omnichannel Communication?

Omnichannel communication is built on a fundamentally different premise from multichannel. In this infrastructure, there are multiple channels, but the customer’s data, interaction history, and preferences sit at the center, and every channel draws from that single source. When a client starts a loan application on your mobile app and connects on a call in the next minute, there is no need to restart the conversation, as due to omnichannel orchestration, your teams can access the entire customer journey easily.

Omnichannel vs. Multichannel: A Side-by-Side Comparison

| Dimension | Multichannel | Omnichannel |

| Center of gravity | The institution | The customer |

| Channels | Multiple channels but siloed | Multiple channels integrated through a central content repository |

| Data | Channel-specific | Unified profile and interaction history |

| Content | Re-authored per channel | One template, rendered across channels |

| Branding & Tone | Drifts by channel | Consistent everywhere |

| Compliance audit trail | Often fragmented | Compliant with time-stamped record |

Where Does Cross-Channel Fit?

Often, cross-channel and omnichannel communication is ambiguous, so it is worth distinguishing between them, as they are not the same. Cross-channel allows customers to move between channels and pick up where they left off, but the data integration underneath it is partial and inconsistent. Omnichannel closes that gap entirely, with full, real-time integration built with compliance requirements in mind from day one.

![]()

Before You Scale Omnichannel, Make Sure the Foundation Is Right

Most CX leaders jump to technology before the six foundational pillars are in place. This guide walks you through exactly what needs to come first.

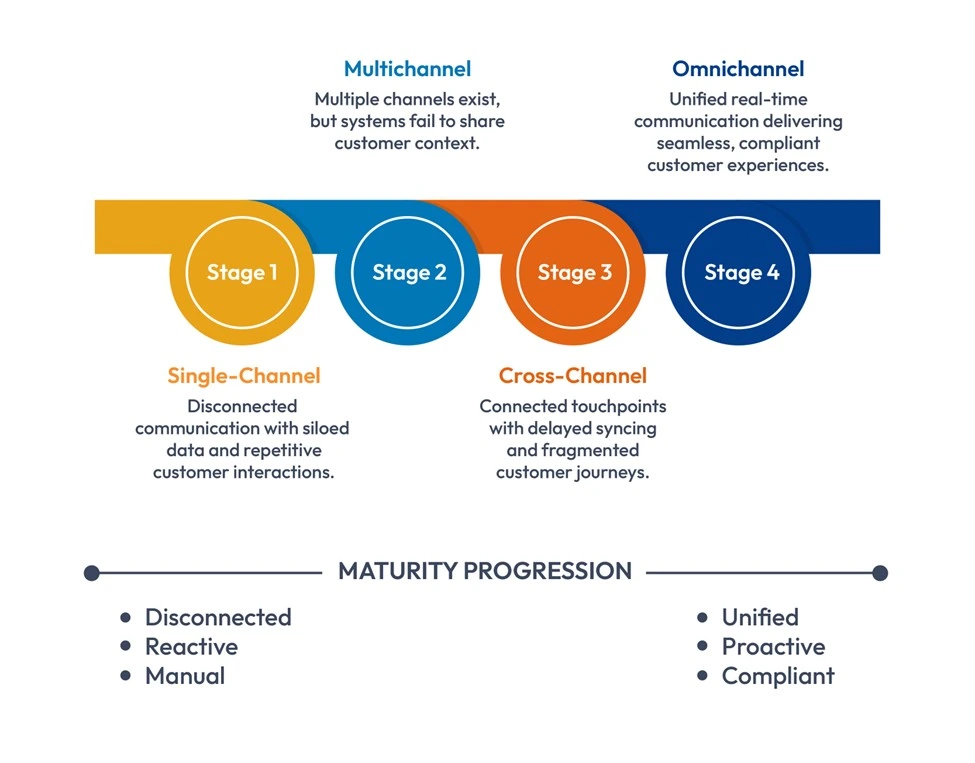

The 4-Stage Customer Communication Maturity Model

Your contact center might look like Stage 4 while your statements, KYC packs, and regulatory disclosures are still running on Stage 2 infrastructure. That disconnect is where the real maturity gap sits for financial institutions, and the four stages below will show you exactly where it is hiding.

Stage 1: Single-Channel

At this stage, communication functions as a one-way street. Whether it is paper statements or branch visits, there is no digital layer connecting them. At this level, a financial services communication strategy is a series of dead ends. Data stays locked in a vacuum, and the customer is forced to restart their story at every turn, resulting in a higher churn rate.

Stage 2: Multichannel

Moving past Stage 1 usually means adding new channels like apps and SMS, but these tools rarely talk to each other. Because the app team and the call center run on different playbooks, they create a “memory loss” experience for the customer. If a client files a complaint on your app and then has to repeat the entire story to a phone agent ten minutes later, you have reached multichannel, but you still lack omnichannel communications banking. At this stage, the customer is the only one bridging the gap between your siloed departments.

Stage 3: Cross-Channel

Institutions that recognize the Stage 2 problem typically invest in connecting their touchpoints, but this is where most firms stall. While a customer can technically move between the app and the branch, the data underneath is usually laggy and incomplete. If a client starts a loan application online but the branch agent is left staring at a blank screen because the status hasn’t synced, the communication layer is fundamentally broken. This is where regulatory risk quietly builds. Without omnichannel journey orchestration, your compliance team is still stuck manually hunting through disparate systems just to reconstruct a basic audit trail.

Stage 4: Omnichannel

Stage 4 is where omnichannel communications banking becomes an operational reality. Unlike the laggy connections in Stage 3, a central omnichannel orchestrator acts as a single brain for the entire institution. This ensures that the document layer and the contact center work in total sync. A business user can update a regulated disclosure once and have it go live across print, email, and the mobile app simultaneously. Because of integrated omnichannel campaign orchestration, the customer experiences one continuous conversation where every digital nudge matches the context of their last branch visit. Most importantly, if a regulator asks for an audit trail, the system pulls a complete record across every touchpoint in minutes.

Why Regulators Are Making Omnichannel a Business Priority

The US Perspective

Since 2022, the SEC has issued over $2 billion in penalties for one main reason: firms cannot prove what and how they communicated to their clients. This usually happens because SMS, email, and call center data are trapped in different systems, making it impossible to pull a single, verifiable record of a customer’s history. Regulators are now specifically targeting these gaps in the audit trail. This fragmentation also creates a massive hurdle for ADA Title II compliance; you cannot guarantee equal access for customers with disabilities if your communication channels aren’t governed by the same central standard.

The EU Perspective

MiFID II Article 16 mandates that firms record and retain all client communications across every digital and physical channel. This requirement is becoming harder to manage as the European Accessibility Act (June 2025) now requires accessibility parity across the entire customer journey. Managing governance independently for each channel is expensive and increases the risk of human error. An omnichannel communications banking infrastructure allows content and governance to sit in one place, making compliance a scalable process rather than a manual task performed before every audit.

Why Most Financial Institutions Think They Are Omnichannel and Are Not

The industry standard for omnichannel is currently limited to the service layer. Strategic investment usually stops once the mobile app, website, and contact center are connected. This leaves the document layer (statements, notices, and disclosures) operating in a vacuum.

These communications represent the highest volume of customer touchpoints and carry the most regulatory weight. Yet, they typically run on infrastructure that has no connection to CRM and other platforms. This disconnect forces a customer to experience two different versions of the same institution: a modern digital front end and a legacy document back end.

If official documents do not sync with real-time digital activity, the strategy is not omnichannel. It is a multichannel environment that lacks a single source of truth. True omnichannel maturity requires the integration of the document layer into the broader customer journey. Without this, the institution remains siloed, regardless of how modern the mobile app appears.

How to Move from Multichannel to Omnichannel: A Practical Roadmap

Step 1: Map Your Top 5 Communication Moments

The first step should be to identify the five interaction points where you think friction hurts most, such as onboarding, statements, servicing queries, disputes, and renewals. Now, for each point, trace every channel it hits and pinpoint exactly where handoffs fail. This audit exposes where multichannel gaps are bleeding revenue and frustrating customers, which will further provide you with clarity regarding where to invest and disinvest.

Step 2: Consolidate Your Content Layer With CCM

This is the foundational step most banks miss. A Customer Communications Management (CCM) platform must be your central engine. Statements, disclosures, and claim letters should originate from one template engine, not four siloed systems. With a CCM platform, a single legal update renders across print, email, SMS, and portals instantly without needing an IT ticket.

Step 3: Unify the Customer Record

Channels cannot operate in isolation. All of your internal platforms must share a centralized content repository. A customer’s preferences and interaction history should be visible to your team at every touchpoint in real time, stopping the need for customers to repeat their story every time they switch from a mobile app to a call center. It is a very crucial step to ensure you deliver a top-notch customer experience.

Step 4: Execute Omnichannel Campaign Orchestration

Once your data and templates are unified, it’s time to stop just sending messages and start orchestrating the entire communication flow. Use omnichannel campaign orchestration to pull personalized insights directly into mandatory documents. This turns a standard monthly statement into a high-engagement vehicle, which accelerates cross-selling and retention.

Step 5: Build Compliance In, Not On

Stop treating compliance as a post-send audit. Every outgoing message needs a time-stamped delivery record from the jump. Given the complex and evolving regulations introduced each year, a unified audit trail is a defensive necessity. Integrating this into your financial services communication strategy is far cheaper than paying for a regulatory failure later.

Step 6: Govern the Content Lifecycle

Establish a single source of truth for every approved content block. When a legal disclaimer changes, it should be updated once in the library and propagate across every channel immediately. This prevents the nightmare of a customer receiving a digital update that contradicts their physical mail.

Step 7: Measure What Actually Matters

Apart from vanity metrics, track channel-of-preference adherence, first-contact resolution, and your regulatory exception rate. These are the hard numbers that prove your financial services communication strategy is actually improving the bottom line rather than just looking good on a slide deck.

Conclusion

The gap between multichannel and omnichannel in financial services is not closing as fast as most institutions think, and the document layer is where that gap is most visible. Customers feel it, compliance teams manage around it, and the cost of leaving it unaddressed compounds over time.

Cincom Eloquence is built specifically for financial institutions navigating this transition. It brings the document layer, the digital layer, and the compliance layer into a single unified architecture, so your communications manager, compliance officer, and IT team can contribute to scaling operations while maintaining accuracy and staying audit-ready without the usual back and forth between systems.

If you are ready to see what that looks like in practice, the next step is a conversation.

FAQs

1. Do we need to replace our entire tech stack to move to omnichannel?

No. Most institutions start by consolidating the content and template layer through a CCM platform without replacing their core banking systems. Omnichannel orchestration works by sitting on top of existing infrastructure and connecting it, not replacing it.

2. What is the ROI of omnichannel in financial services?

The returns show up in three places: reduced complaint volumes, lower compliance remediation costs, and higher product holdings per customer. The omnichannel vs. multichannel communication gap is not just a customer experience issue; it directly affects revenue and risk exposure.

3. How do we get internal buy-in from IT and compliance teams?

Frame it around their biggest pain points. For IT, it is about reducing the number of systems they are maintaining. For compliance, it is about having a single audit trail instead of reconciling records across multiple platforms. Omnichannel communications banking solves both problems simultaneously.

4. How does omnichannel handle customers who still prefer physical channels like branches?

A genuine omnichannel architecture treats the branch as one channel among many, not a separate operation. Whatever happens in the branch updates the unified customer profile in real time, so every other channel reflects that interaction immediately.

5. Can omnichannel work with legacy core banking systems?

Yes, provided the integration layer is built correctly. A CCM platform acts as the connective tissue between legacy systems and modern digital channels, which means institutions do not need a full core banking replacement to start delivering a connected customer experience.

6. How much does moving to omnichannel actually cost?

The more relevant question is what staying multichannel is already costing. Duplicate content teams, manual compliance reconciliation, customer churn from fragmented experiences, and regulatory penalties from incomplete audit trails all carry a price that compounds every year the transition is delayed.