Introduction

California’s privacy law has changed. For financial institutions, this is not something you can push down the road.

On 23 September 2025, the California Privacy Protection Agency signed off on a new set of regulations under the California Consumer Privacy Act (CCPA). The first set of obligations went live on 1 January 2026. After that, more requirements are scheduled to come in through 2027 and 2028. So, in practice, this is going to keep evolving for a while.

If you’re a financial institution whose functions range across banking, lending of funds, fintech, or investments, you’re already dealing with the impact because these businesses handle a lot of sensitive customer data, and therefore, they depend on automated decisions in everyday processes. They also work with layers of third-party vendors, sometimes more than they can fully map. Putting all of this together, the scope becomes pretty wide, pretty quickly.

Which is why this isn’t just a compliance update sitting with one team in the background. It affects how work actually gets done. It shows up in operations, in systems, and especially in how institutions handle CCPA 2026 financial institutions’ requirements in customer communications.

This article walks through what’s changing, where it starts to matter in real terms, and what you should be thinking about next.

What Changed on 1 January 2026: Customer Communication Implications

The January 2026 changes show up most clearly in three areas: how institutions respond when customers exercise their rights. How consent is presented across digital interfaces and what privacy policies now need to spell out.

Confirming Opt-Out Requests

One of the biggest and immediate shifts this year is around something that used to be an easy miss, which is acknowledgement. After the rollout, the handling of opt-out requests is beyond the ambit of the back-end. It’s more focused on closing the loop with the customer, so they’re not left guessing. They can see that their choice was received and acted upon.

Earlier, when a customer opted out of data sharing, the request would just disappear from their view. It went through the system; it may have been processed correctly, but from the customer’s side, there was no real signal or clarity regarding the request. They were expected to trust that it worked.

However, after the new rollout, this approach doesn’t hold anymore. Now, when a customer opts out, the financial institutions need to make sure that the response is visible. It could be a toggle in a banking app. It could be a browser-based signal. Either way, the institution has to confirm what exactly happened, clearly and immediately.

![]()

Compliance Without Compromise: Modernize Customer Communications

Learn how modern systems cut regulatory risk, streamline workflows, and deliver personalized customer experiences in one solution.

Responding to Data Access Requests

The previous 12-month limit for data access requests has been replaced by a much wider window. If a lender or a bank retains personal information, then they must now be able to retrieve and present that data going back to January 1, 2022, if a customer requests.

For many firms, this means that data, which was once considered buried in long-term archives or legacy databases, is now active and discoverable. When a customer asks to see their history, the institution must be able to pull those records and present them clearly. It is a transition from keeping records for the bank’s benefit to keeping them for the customer’s oversight.

What Privacy Policies Must Now Say

The language of privacy policies is also undergoing a necessary modernization. For too long, financial institutions have used broad terms like “third parties” to describe a complex web of partners. Under the 2026 rules, this lack of detail is unacceptable going forward. Documents must list the following categories separately:

- Service Providers: Entities that process data only for the institution’s specific business needs.

- Contractors: Partners with a direct contract for specific tasks.

- Third Parties: Entities that may use the data for their own independent purposes.

This level of detailing is vital because the vendor landscape for a modern bank is vast, ranging from credit bureaus and fraud detection systems to cloud platforms. By separating these categories, financial institutions finally give customers a realistic map of where their information goes, supporting CCPA compliance in banking communications across all interactions.

The Principle of Choice Symmetry

Perhaps the most visible change is the move toward interface equality, or symmetry. It might seem that this doesn’t carry much weight, but in reality, it does. The law now clearly recognizes that a choice is not truly a choice if one option is hidden or harder to reach. This shift is especially important for CCPA 2026 financial institutions, which must ensure that consent mechanisms meet the new standards.

This means the end of the “dark pattern,” for instance, those subtle design tricks like making a “decline” button smaller or greyed out compared to a bright “accept” button are strictly restricted now, both the “accept” and “decline” button should be in the same color, same font, and same pattern, i.e., symmetry.

Also, consent now requires clear, affirmative action, which indicates that closing a pop-up or ignoring a banner is no longer enough to claim that a customer has agreed to share their personal information with the financial institutions.

Handling Sensitive Information for Younger Consumers

Finally, the 2026 standards have raised the stakes for youth-focused banking. By classifying all data from consumers under the age of 16 as sensitive, the law forces a change in how student loans and youth savings accounts are managed.

When an institution collects this data, it cannot simply point to a link at the bottom of a webpage. They must provide a notice and a control (such as a toggle switch) at the exact point of collection. Whether it is a mobile app or a physical kiosk in a branch, the tools to limit data use must be right there, in the hands of the young consumer.

How Financial Institutions Should Navigate the New Privacy Dialogue Under CCPA

Start with clarity. Everything else follows

The very first step is to bring clarity. Most institutions still overcomplicate privacy communication. Legal language creeps in, sentences get longer, and the message gets buried somewhere in the middle. That approach will not work anymore. If customers have more control over their data, they should be able to understand that without effort. Clear, direct language does more than simplify compliance. It signals intent. It shows that the institution is not trying to hide behind complexity.

Consistency is where trust is built or lost

Customers don’t experience your institution in one place. They move between apps, calls, and in-person interactions without thinking about it. So, when the tone shifts or the message changes slightly, it stands out for customers, and they do notice. For instance, information about limiting data sharing should feel the same everywhere with the same tone, same clarity, and same level of reassurance, irrespective of the channel the customer is using. That consistency does more than tidy up communication. It builds a sense that the institution is in control and aligned internally.

Timing matters more than volume

There’s a tendency to pack everything into a privacy policy and call it done. Most customers never read it, and even when they do, it’s rarely at the right moment. What actually works is much simpler. Give people information when they need it. During a loan application. At the point of data sharing. In the exact moment a decision is being made. That’s when it lands, and that’s when it helps.

Design is not decoration. It’s a signal.

Customers notice more than institutions assume. If one option is highlighted and the other is harder to find, the message is clear. If both choices are presented evenly, that sends a different signal. Neutral colors. Balanced buttons. Clean layouts. These are small decisions, but they carry weight. They show whether the institution respects choice or is quietly steering it.

Lead the conversation instead of waiting for it

Most institutions still wait for customers to dig into settings or read updates on their own. That’s a missed opportunity. Privacy changes should be surfaced, not buried. A simple note in an app update. A short message explaining what’s new and why it matters. Nothing heavy, just enough to make the customer aware. Handled well, this shifts perception. It stops being about regulation and starts feeling like a service. The institution comes across as deliberate, transparent, and in control of how it handles personal information.

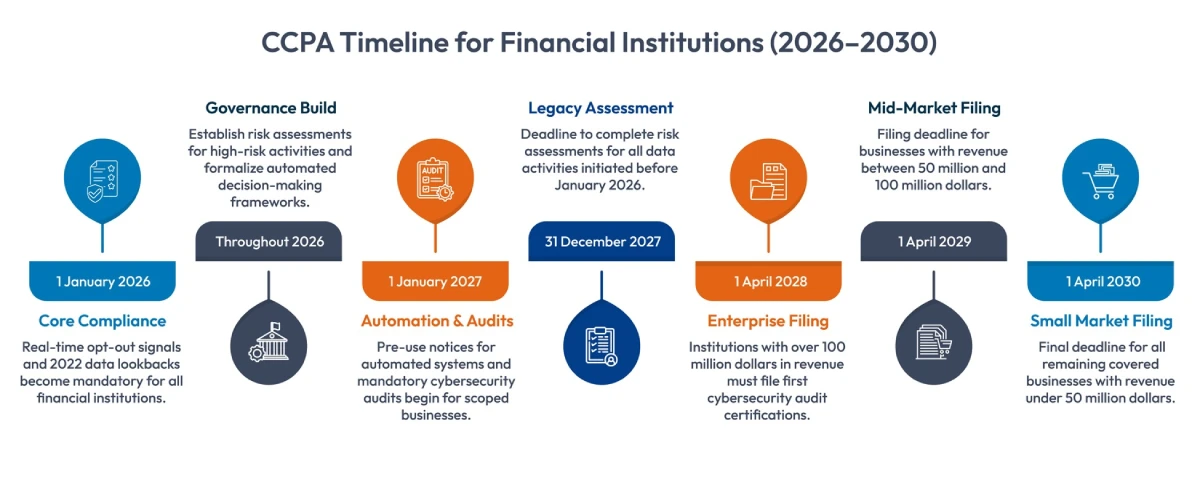

CCPA 2026 for Financial Institutions: A Phased Transition

For financial institutions, CCPA 2026 is easier to follow as a timeline rather than a single deadline. The first phase brings changes to customer rights and communication touchpoints, but the work doesn’t stop there.

Through 2027, the focus will shift toward risk assessments, automated decision-making, and audit readiness. From 2028 onward, these efforts will move into formal filings and certifications.

For teams working on CCPA compliance in banking communications, this progression shapes how priorities are set and how systems need to evolve.

The timeline shows how expectations build year by year, not all at once. Institutions that plan for the later phases early tend to avoid repeated rework.

Preparing for CCPA 2026 and Beyond

CCPA 2026 brings multiple deadlines that stretch through 2030. Customer rights, opt-out confirmations, audits, risk assessments, and many more such requirements sometimes create complexity that touches every part of a financial institution. Therefore, adhering to these requirements takes more than policies; it requires a clear and reliable system to manage communications with accuracy and transparency.

Cincom Eloquence gives financial institutions control. It uses if-then logic to deliver notices at the right moment, maintains a single source of truth, tracks versions, and provides audit-ready trails across email, mobile apps, statements, branch interactions, and many more features that can make your communication workflow easy to execute. Every communication reflects the customer’s choices and regulatory requirements without manual effort.

With Cincom Eloquence, you can manage compliance confidently, maintain trust with customers, and stay prepared for evolving CCPA obligations and other such regulations as well.

![]()

Take Control Today

Stay ahead of CCPA 2026 with clear, consistent, and traceable customer communications.

FAQs

1. What does CCPA 2026 mean for financial institutions?

CCPA 2026 requires financial institutions to provide visible acknowledgements of customer rights, expanded data access, and transparent privacy policies.

2. How should banks update their customer communications for CCPA compliance?

To meet CCPA compliance banking communications requirements, banks must ensure all communications reflect current customer rights, consent choices, and sensitive data handling.

3. Can we still use X-out or click-away behavior as implied consent?

No. Under 2026 standards, if a user closes a consent banner without clicking an affirmative accept button, it must be treated as a non-consent. Silence or inaction no longer constitutes valid permission for data sharing.

4. How can financial institutions manage extended data access requests?

CCPA 2026 extends the lookback period to January 1, 2022. Institutions need centralized systems to quickly retrieve and deliver historical communications.

5. Can technology help institutions achieve CCPA compliance?

Yes. Platforms like Cincom Eloquence help financial institutions automate rights acknowledgements, maintain audit trails, and enforce consistent communication across channels.