Introduction

If trust is the ultimate currency in financial services, then everyday operational communications are where that currency is either earned or spent. For years, institutions measured the success of these interactions through simple dispatch volumes and open rates. But delivery confirmation only proves that a file left a server. It does not mean a customer understood the message or knew what to do next.

This gap becomes obvious during critical onboarding and compliance workflows. When a regulatory disclosure arrives late, fails to render properly on a smartphone, or uses confusing language, customer trust fractures. The immediate result is account abandonment, leaving internal teams to manually clean up the damage.

In 2026, forward-thinking institutions are shifting their strategy toward comprehensive financial services benchmarking. Instead of checking just basic delivery logs, teams are tracking real-time comprehension, mobile rendering quality, and onboarding completion rates. Prioritizing these metrics is foundational to modern customer experience management in banking. This guide breaks down the modern performance standards teams are using to eliminate friction, protect revenue, and turn standard notifications into verified trust builders.

What Is Financial Services Communication Benchmarking?

Financial services communication benchmarking is the systematic process of measuring how effectively an institution delivers, tracks, and optimizes regulated and marketing messages against industry performance standards. Rather than tracking delivery volume alone, this methodology evaluates the entire document lifecycle to ensure outbound communications actively engage customers while maintaining strict regulatory compliance.

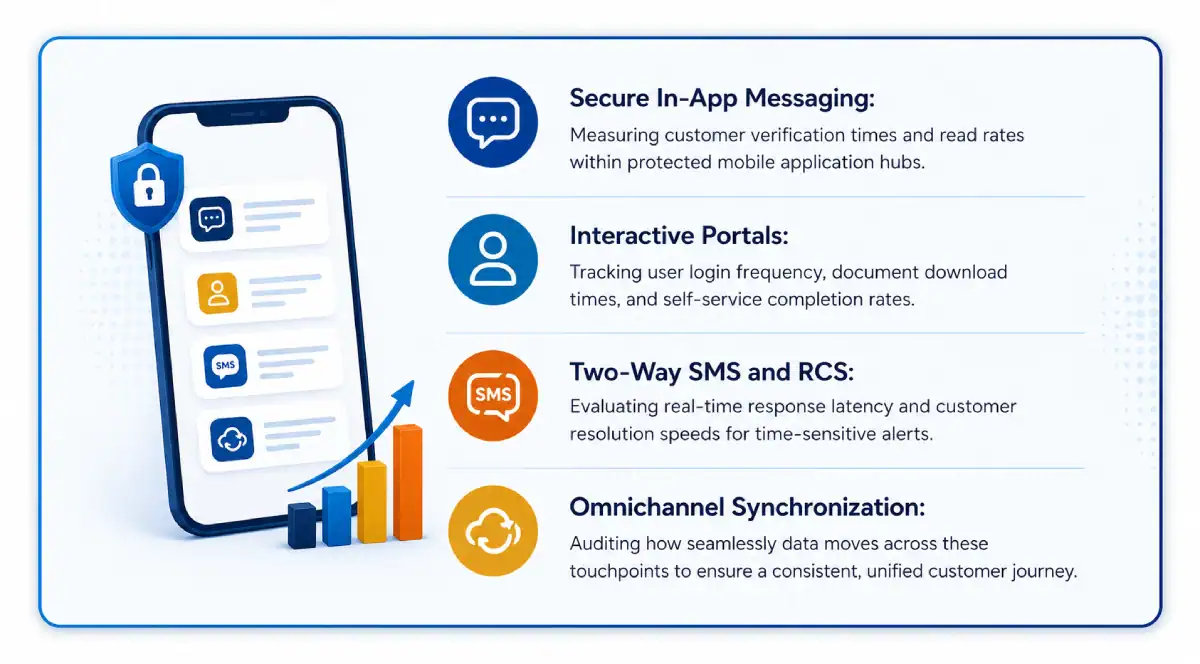

The 2026 operational scope requires organizations to look past traditional distribution and benchmark financial services against the capabilities of modern, agile platforms. It focuses heavily on tracking performance across a dynamic ecosystem designed to reduce friction:

Banking Communication Checklist: Identify Compliance and Governance Gaps Early

Assess communication workflows, disclosure accuracy, audit readiness, and cross-channel consistency before gaps create regulatory risk.

The State of Customer Communications in Financial Services in 2026

The structural challenge of financial communications in 2026 is balancing two distinct operational speeds. Institutions have done an incredible job building hyper-fast, mobile front ends. The bottleneck now lies in engineering backend infrastructure to match that exact same velocity, ensuring document generation and compliance delivery flow seamlessly into the digital channels users prefer.

The Mobile Frontend vs. Backend Disconnect

54% of retail consumers now utilize a mobile app as their primary banking channel (ABA).

47% of digital account openings are abandoned mid-process (Capgemini).

The data shows that front-end mobile demand is mature, but scaling the underlying document infrastructure remains a complex engineering challenge. When nearly half of prospective clients depart an onboarding process midway, it highlights a need to align automated data verification with the speed of the user interface.

The Identity and Context Loss Problem

86% of banking executives are actively prioritizing omnichannel orchestration (Capgemini).

The fact that 86% of executives are prioritizing orchestration shows the industry is actively working to build a unified digital memory. Right now, data often sits in siloed applications. If a user initiates a form on a smartphone but needs to transition to a laptop to upload a tax statement, preserving that context is vital. Eliminating the need to restart a process from scratch across portals, apps, and branches is one of the highest-leverage improvements available for customer experience management in banking.

The Compliance Challenge of Machine Filtering

In 2026, the major shift we have seen is that the human inbox has reached maximum capacity. To manage notification fatigue, consumers are increasingly deploying personal AI assistants to filter and screen their incoming digital environments.

When mandatory disclosures, privacy updates, or fraud alerts are delivered as static, unformatted text blocks, these automated agents flag them as noise and block them. To ensure regulatory notices actually reach the consumer, outbound communications must be formatted into highly structured, machine-readable data. This allows automated filters to parse compliance notifications accurately, ensuring the end-user stays contractually notified.

5 Key Metrics Financial Institutions Should Benchmark

Having analyzed the operational and compliance shifts shaping modern distribution channels, the next step is establishing clear frameworks to measure performance. Transitioning from theory to predictable execution requires moving past surface-level telemetry. To operationalize financial services benchmarking, organizations must track specific operational indicators that tie backend efficiency directly to user behavior and mitigate the risk of machine filtering.

#1. Communication Delivery Speed

Benchmark the exact time-to-delivery for critical transactional documents, such as loan approvals, claims notices, and trade confirmations.

- How to implement: Measure the time elapsed from the moment a core system triggers an event to the millisecond the notification is generated. Eliminate processing latencies to ensure immediate delivery. Fixing this backend bottleneck directly prevents the frontend journey abandonment and user drop-off discussed previously.

#2. Customer Engagement Rates

Evaluate deep interaction metrics rather than relying on surface-level email open rates. True customer experience management in banking depends on tracking how users actually interact with outbound data.

- How to implement: Monitor average session duration and specific document view rates on digital statements. If data reveals high open rates but zero-second view times, the document layout is causing immediate cognitive fatigue. Simplify text architecture to lower the reader’s cognitive load and extend engagement.

#3. Digital Adoption and Channel Usage

Track the percentage of customers actively opting for digital-first delivery channels versus traditional paper mail.

- How to implement: Segment your user base by communication preferences and map delivery success across channels. Identify friction points in the digital onboarding flow that cause users to revert to physical mail. High digital adoption directly correlates with clear, mobile-optimized layouts that remove user doubt and friction.

#4. Compliance and Audit Readiness

Measure the total processing time required to retrieve, verify, and report historical communications during regulatory audits.

- How to implement: Run quarterly audit simulations. Track the time required to pull unedited, historically accurate versions of specific customer notifications along with delivery metadata. Seamless retrieval reduces operational risk and ensures continuous compliance readiness.

#5. Machine-Parser Success Rate

Audit the frequency of delivery successes, template inaccuracies, or formatting errors, specifically tracking how effectively data is parsed by external filters.

- How to implement: Monitor the ratio of successful delivery cycles against system errors. Ensure outbound communications are formatted as highly structured, machine-readable data rather than flat, static text blocks. High machine-parser success rates ensure that critical regulatory notifications successfully clear automated screening tools and actually reach the end-user. Leadership teams must continuously track this metric to effectively benchmark financial services communications against evolving AI filtering behaviors.

Common Benchmarking Gaps Across Financial Institutions

Identifying performance indicators is meaningless if underlying organizational constraints compromise data collection. When institutions fail to establish accurate baselines, it is typically due to three structural gaps:

Siloed Data Sources

- The Gap: Legacy architectures separate core business systems (such as loan origination, CRM, and billing engines) into distinct data repositories.

- The Impact: This fragmentation prevents a unified view of the customer journey. Without a single data layer, teams cannot track the end-to-end delivery speed of a single disclosure or statement across multiple touchpoints.

Manual Communication Workflows

- The Gap: Many organizations remain dependent on manual IT ticketing queues or physical sign-offs to execute simple template changes and compliance updates.

- The Impact: This operational dependency creates severe processing bottlenecks and introduces human error into variable data fields. It actively impedes agility, making it impossible to adapt quickly to changing regulatory demands.

Limited Analytics and Reporting

- The Gap: Internal visibility frequently stops the moment a file is generated, leaving the organization blind to downstream delivery performance.

- The Impact: Without post-generation telemetry, institutions cannot track document view rates or machine-parsing success. This leaves teams completely blind to actual user engagement and vulnerable to automated AI filters.

How a Customer Communication Management Platform Improves Benchmarking and Visibility

Overcoming operational gaps requires migrating from legacy infrastructure to a centralized software layer. A modern customer communication management platform resolves visibility limitations through three core capabilities:

4 Quick Steps to Build a Reliable Benchmarking Framework

A phase-by-phase approach is required to easily shift towards an advanced communication setup. Financial firms can look at four distinct steps to get a reliable financial services benchmarking process off the ground:

- Map out what exists right now

Document the current architecture without overcomplicating it. You need to know exactly where old tools, disconnected software, and siloed departments are blocking full visibility into your data. - Pin down your baseline numbers

Get an honest look at performance before changing any code or systems. This means calculating current document delivery speeds, tracking error rates, and determining the actual per-channel costs to see exactly where the floor is. - Find the right competitive peer group

Contextualize your findings. Compare those baseline figures against institutions with similar asset sizes, regulatory rules, and operational setups. Seeing where you lag reveals immediate ways to protect and improve customer experience management in banking. - Shift to an automated feedback loop

Stop treating reviews as a once-a-year manual project. Deploying centralized tech turns this into an ongoing operational loop, giving teams a real-time look at changing consumer habits and machine-filtering roadblocks as they happen.

Conclusion

The ledger of customer trust is balanced in the quiet minutiae of daily operations. Every automated alert or routine statement sent out is either a quiet deposit or a steady withdrawal from that established account. When a technical glitch or an unparsed data block interrupts this flow, it is an immediate erosion of that core relationship.

Looking ahead, the operational landscape demands absolute transparency. The institutions that successfully insulate themselves from attrition do so by looking honestly at their delivery pipelines, transforming raw document generation into a highly visible, measurable strategic asset. Centralized communication engines, such as Cincom Eloquence, provide the exact blueprint needed to bridge legacy backend systems with modern distribution layers, ensuring every digital interaction remains flawless.

Refining a financial services benchmarking strategy ultimately comes down to accountability. When the data moving between an institution and a consumer is clear, accurate, and completely auditable, trust becomes a tangible, predictable asset. To secure long-term account retention, you need to make sure that every single outbound transmission serves as undeniable proof of operational reliability.

Schedule a demo to see how centralized customer communication platforms help financial institutions improve benchmarking visibility, compliance tracking, and delivery performance.

FAQs

1. Beyond open rates, what actual metrics should our analytics team look at first?

Focus on average session duration and document view rates within your digital portals. Open rates only prove a message landed; tracking how many seconds a user spends on a digital statement tells you if the text architecture is causing cognitive fatigue or driving real engagement.

2. How do automated AI filters change how we format regulatory notices?

Personal AI assistants block unformatted text blocks as digital noise. To bypass these automated filters, notices must be converted into highly structured, machine-readable data layers so the consumer’s automated tools can parse and deliver the compliance information.

3. Why are our legacy backend systems creating a barrier to accurate operational benchmarks?

Siloed architectures keep billing, CRM, and loan systems separate. Without a centralized communication layer connecting these environments, it is impossible to map the end-to-end customer journey or measure true delivery speed across different business lines.

4. Realistically, what is customer experience management in banking from an operational standpoint?

It is the practice of auditing and optimizing every digital touchpoint to remove friction. Operationally, this means turning dry compliance data, statements, and automated notices into clear, mobile-optimized interactions that protect institutional trust.

5. What are the best solutions for customer experience management in banking to fix delivery gaps?

The most effective approach is deploying centralized software platforms like Cincom Eloquence. Cincom Eloquence bridges legacy backend architectures with modern delivery channels, providing the centralized analytics and end-to-end tracking needed to guarantee reliable performance.