Introduction

Mortgage origination satisfaction in the US hit a record high in 2025, while mortgage servicing satisfaction hit an all-time low that year, scoring 131 points below origination in J.D. Power’s annual study.

The ironic part of the above-mentioned data is that it represents the exact same borrower and the exact same loan, but two completely different experiences. When a borrower is buying a house, the communication is seamless. The lender texts updates, walks them through every step, and treats them like a valued client. However, the moment the loan is approved and moves to the servicing lifecycle, that dynamic changes.

A big part of this gap comes down to communication continuity. Most borrowers do not interact with their loan provider regularly. Aside from payment reminders, escrow-related notices, or loan transfer communications, there are often long gaps with no meaningful engagement. When communication does happen, the message that arrives by email often contradicts what the call center said, which, in turn, differs from what showed up in the post.

Omnichannel borrower communication is the practice of fixing this disconnect. It ensures that every message, across every channel, feels like it is coming from a single organization that knows exactly who the borrower is and where they stand in their loan journey.

This blog explores seven best practices for omnichannel borrower communication in loan servicing. It covers practical ways to create consistent borrower experiences across channels, common operational challenges servicing teams face, and the architecture required to support omnichannel communication at scale.

#1: Map Communication to the Loan Lifecycle, Not Just to Channels

Channel strategy gets a lot of attention in borrower communication, but the more foundational problem is that most servicing teams have not defined what they actually need to communicate and when. The channel question comes later. The first question is about moments.

A borrower in the first month of their loan has different needs than someone who is three payments behind. Both are different from a customer navigating a servicing transfer they found out about two weeks ago. These are distinct communication moments, and they need to be treated as such.

The practical fix is a lifecycle communication map. Go through the loan journey and pin down what needs to go out at each stage as part of your loan servicing communications strategy:

- Onboarding: welcome message, payment setup confirmation, portal access

- Active servicing: escrow updates, rate change notices, annual statements

- Delinquency: early outreach, hardship options, loss mitigation notices

- Servicing transfer: advance notification, new payment instructions, grace period confirmation

- Payoff: final balance and lien release confirmation

This map is also what makes omnichannel communication execution actually possible. With it, you can make deliberate decisions about which channel carries which message and ensure a borrower moving from a portal notification to a phone call to a mailed notice is receiving a consistent experience, not three different versions of the same situation.

![]()

Omnichannel Communication at Scale: A Guide for CX Leaders

Discover the strategies, governance, and technology needed to deliver seamless customer experiences.

#2: Capture Borrower Channel Preferences and Actually Use Them

Channel preference data exists in almost all financial institutions. It is collected at origination, stored somewhere in the CRM, and largely ignored after that. Even after having such information, often the borrower who opted out of paper mail gets paper mail, while the customer who opted for SMS gets an email.

The problem here is not about collection (since you already have the information); it’s about activating the flow. To fix this, preferences need to be:

- Captured at onboarding and updated at every meaningful interaction

- Stored in a single centralized location, not siloed across systems

- Connected to every outbound channel: servicing platform, print vendor, email, and SMS gateway

- Reviewed periodically because borrower preferences change over time

Without such infrastructure, the idea of omnichannel borrower communication breaks down entirely. Preferences sit in a CRM doing nothing while borrowers receive communications through channels they never asked for, further leading to distorted trust among them.

For EU-based servicers, this is not just a CX problem because under GDPR, how you capture and honor communication consent carries legal weight.

#3: Build Compliance into the Communication Workflow

Don’t treat compliance as a final checkpoint. Usually the process follows: the template gets created, the operations team reviews it, the legal team approves it, and it goes out; however, this workflow has a ceiling. When loan volumes grow, when regulations change, or when someone on the ops team produces a one-off notice outside the review cycle, things break. Multiple versions of the same notice end up in circulation across different channels, and nobody is quite sure which one is current. That is the opposite of what omnichannel communication demands.

The stronger approach is to embed compliance logic directly into the communication template from the start, not in the review process around it:

| Communication Type | Regulatory Requirement |

| Delinquency notice | Live contact by day 36, written by day 45 (Reg X) |

| Loss mitigation | Acknowledgment within 5 business days (Reg X) |

| Adverse action | Written notice with specific reason codes (ECOA) |

| Servicing transfer | 15 days’ advance written notice (RESPA) |

| Periodic statements | Specific fee descriptions required (Reg Z) |

When compliance lives in the template, communication stays consistent across every channel, audit trails stay clean, and the review bottleneck shrinks considerably. Combined with loan document automation, this approach helps servicers maintain regulatory consistency while scaling their omnichannel communication framework.

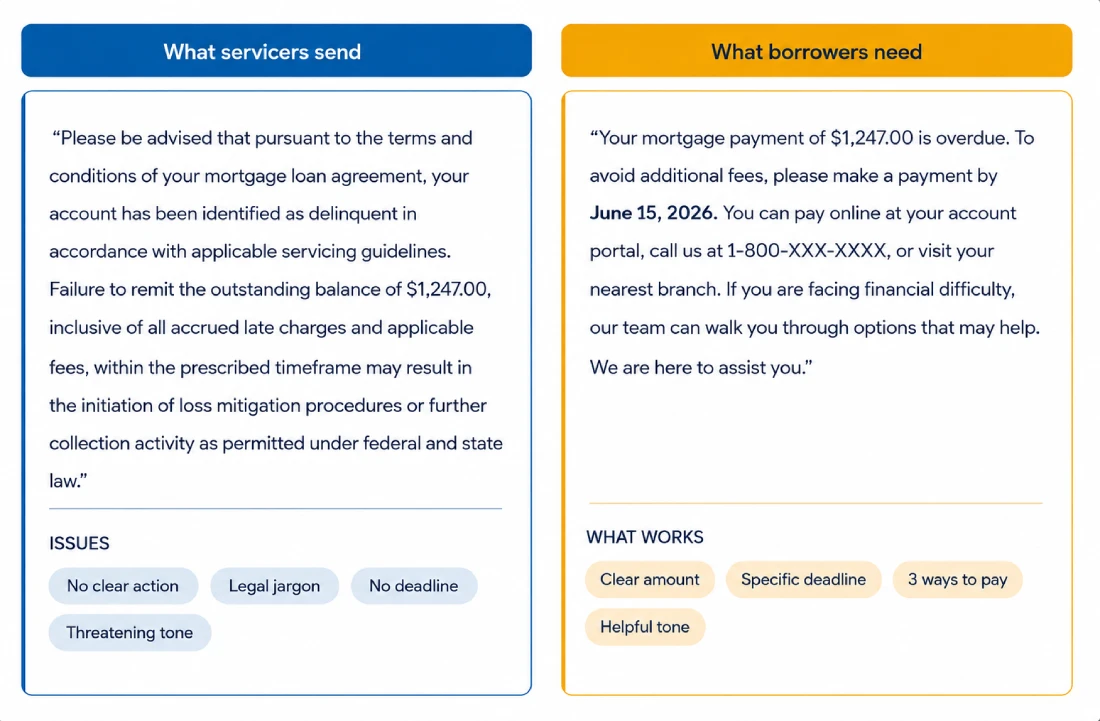

#4. Write Borrower Communications That People Can Actually Act On

The entire premise of omnichannel borrower communication rests on one thing: the borrower understanding what they received and knowing what to do next. For instance, a notice distributed across email, SMS, and post but leaves the borrower confused and has not solved anything means you have just distributed the confusion more efficiently. Effective loan servicing communications should create clarity and drive action, regardless of the channel used.

Over 25.7 million people in the US have limited English proficiency, and the European Accessibility Act sets clear expectations around digital communication accessibility for EU-based institutions.

A few deliberate choices make a significant difference:

- Lead with what the borrower needs to do, not with the legal context behind it

- Offer multilingual versions for high-volume languages in your borrower portfolio

- Test communications with real borrowers before rolling them out across channels

#5: Keep the Message Consistent Across Every Channel

Channel silos are the most common reason omnichannel communication breaks down in practice. The email team owns email templates, the print vendor manages mailed notices, and SMS is handled by a separate operations team. Nobody owns the message itself, and over time each channel drifts.

The result is a borrower who receives a payment reminder by SMS, a slightly different version of the same notice by email, and a third variant by post. From the borrower’s perspective, it looks like three different organizations are managing their loan.

Fixing this requires centralizing template ownership, not channel ownership. One system should maintain a central repository of all templates, flows, and communications, and all channels should pull from that single source:

- Consistent language and tone across email, SMS, post, and portal

- Single approval workflow for any template change

- Version control so outdated templates cannot circulate across channels

# 6: Personalize Beyond the Borrower’s Name

Most borrower interactions start and end with a first name in the greeting. That is not personalization. Real personalization in loan servicing communications means shaping the communication itself based on what is actually known about the borrower.

A first-time homeowner three months into their mortgage needs different communication than a long-term customer with a clean payment history approaching payoff. Loan type, lifecycle stage, payment behavior, and channel preference are all available data points that most servicing teams collect but do not use much to shape outbound personalized communication.

Putting that data to work means:

- Tailoring message content based on loan type and stage

- Adjusting tone and frequency based on payment history

- Surfacing relevant options like refinancing or hardship programs at the right moment

- Delivering that personalized message through the borrower’s preferred channel

Omnichannel communication without personalization is just noise delivered consistently.

#7: Measure Your Communication

An omnichannel borrower communication framework is incomplete without a measurement layer. Knowing that a message went out is not the same as knowing it worked, and at scale that distinction matters more than most servicing teams realize.

The metrics worth tracking fall into six categories:

| Category | Metric | Why It Matters |

| Delivery | Email open rate, SMS response rate, portal login after notice | Shows if the message reached and engaged the borrower |

| Operational | Inbound call volume by communication type, call deflection rate | Identifies which notices are generating confusion |

| Compliance | Reg X timeline adherence, acknowledgment turnaround | Documents that regulated communications went out on time |

| Borrower Experience | Complaint rate, repeat contact rate, satisfaction scores | Surfaces where the communication experience is breaking down |

| Channel Performance | Engagement rate by channel, loan stage, and borrower segment | Shows which channels are actually working and for whom |

| Content Effectiveness | Templates generating the most follow-up calls | Flags clarity issues before they become complaints |

Tracking these metrics turns omnichannel communication from a paper strategy into a measurable, continuously improving business function. These insights can also help organizations identify opportunities to strengthen loan document automation and improve communication efficiency across channels.

The Operational Challenges of Omnichannel Communication

The seven best practices for omnichannel borrower communication in loan servicing sound straightforward on paper. But when you sit down to implement them across a live servicing operation, you run into real infrastructure walls. Here is where teams typically get stuck.

System Silos

The core servicing platform and the CRM rarely talk to each other in real time. This means the borrower data feeding your outbound communication is incomplete. A system might trigger an automated email based on a loan milestone without “knowing” that the borrower called the contact center yesterday to resolve that exact issue.

IT Dependency

In many legacy setups, business users cannot touch communication templates without going through IT. Every minor copy tweak, regulatory update, or format adjustment requires an IT ticket. That queue does not move at the speed modern servicing communication requires.

Multi-State Regulatory Variation

Servicing loans across multiple states means managing dozens of variations for a single letter type. Different states require different disclosure language, distinct timing rules, and specific formatting. Managing these rules through separate, static templates does not scale.

Legal Bottlenecks and Accessibility

Template changes often get stuck in legal review for weeks because compliance teams lack a clear way to audit changes quickly. At the same time, digital communications must meet WCAG accessibility standards in the US and the European Accessibility Act (EAA) in the EU, yet most teams lack an automated way to verify compliance before a message goes out.

The CCM Infrastructure Layer That Makes Omnichannel Communication Work

The challenges above have a common thread. They are not communication problems; they are infrastructure problems. The message is not the issue; it is the system behind the message that is breaking down.

A Customer Communications Management platform (CCM) is built specifically to address this. It sits across your existing servicing stack and acts as the single layer where all borrower communication is created, managed, and delivered across every channel.

Here is what that looks like in practice:

- Business users can create and update templates without raising an IT ticket.

- Compliance logic and regulatory variations are embedded directly into templates, so the right version goes out to the right state automatically.

- All channels (email, SMS, post, and portal) pull from one centralized content source, keeping messaging consistent across every touchpoint.

- CCM integrates with your existing servicing systems through API-based connectors, pulling borrower data into one place and enabling personalization at scale without rebuilding your tech stack.

For financial services organizations managing high volumes of regulated borrower communication, CCM is what turns the seven practices in this blog from aspirational to operational.

See Cincom Eloquence in Action

Managing omnichannel borrower communication at scale requires the right infrastructure. Cincom Eloquence gives communication teams direct control over every borrower touchpoint across every channel.

Request a demo to see it in action.

FAQs

1. How Do Modern Compliance Regulations Impact Omnichannel Borrower Communication?

Regulations govern not just what you say to borrowers but when, through which channel, and in what format. For servicers operating across the US and EU, meeting those requirements consistently across every channel is one of the core challenges of omnichannel borrower communication.

2. Why is Fragmented Data the Biggest Bottleneck in Loan Servicing Communications?

When borrower data is spread across systems that do not sync, loan servicing communications break down. The right message goes out at the wrong time, personalization fails, and borrowers receive notices that do not reflect their actual loan status.

3. What is an audit trail in borrower communications?

A timestamped record of every communication sent to a borrower, including what was sent, through which channel, and when. In a regulated environment, it is what proves compliance when a dispute arises.

4. How Does Customer Communications Management (CCM) Software Modernize Loan Servicing?

CCM software brings loan document automation, template management, compliance logic, and multichannel delivery under one roof, giving servicers a single layer of control over every borrower touchpoint.

5. How does a CCM platform integrate with existing loan servicing systems?

Through API-based connectors that pull borrower data from your servicing, CRM, and origination systems into one place, enabling personalized omnichannel communication without rebuilding your tech stack.

6. Can business teams manage loan servicing communications without relying on IT?

Yes. CCM platforms give business users direct control over templates, content updates, and workflows through a no-code interface, so regulatory updates and channel changes do not need an IT ticket.