Every complex system depends on a framework of controls that preserve order as scale increases. In small organizations, oversight is often personal and direct. As institutions expand, processes multiply, responsibilities are distributed across teams, and systems begin to operate at a volume no individual can fully supervise. At that point, governance depends on structure rather than intention.

Banking operates at precisely this level of complexity. Financial products vary across jurisdictions, regulatory obligations evolve continuously, and millions of customer communications are generated each month across digital and physical channels. Each of those communications carries legal significance.

Supervisory authorities such as the Federal Reserve and the European Banking Authority evaluate whether institutions maintain reliable control over these outputs. That evaluation depends on evidence of governance embedded within the communication lifecycle itself.

Customer Communication Management addresses this structural requirement. It provides a controlled environment in which regulated content is authored, approved, versioned, distributed, and archived according to defined rules. In doing so, it strengthens compliance not through oversight alone, but through systemized execution.

Here are eight ways CCM strengthens regulatory compliance in banking and why it matters for both the institution and the customer.

#1. Enforcing Governance Through Centralized Template Control

Governance weakens when communication templates are owned by multiple teams, stored across disconnected systems, and updated through informal coordination. In that environment, regulated language can drift over time. A clause revised for one product line may remain unchanged in another. A disclosure updated for one jurisdiction may not propagate across channels. The exposure is structural.

CCM addresses this at the template layer itself.

-

Role-based access controls

Authoring rights, review authority, and publishing permissions are clearly defined within the system. Compliance teams approve regulated language. Business teams cannot independently alter master disclosures without triggering workflow controls.

-

Structured approval workflows

Templates move through predefined review paths before release. Legal, compliance, and product stakeholders validate changes inside the platform. Every approval is recorded with the user identity and timestamp.

-

Locked master templates

Core disclosure components are maintained as controlled content blocks. These blocks cannot be edited at the channel level. When updated centrally, they synchronize across all dependent communications.

-

Audit-ready repositories

Every template version is preserved with effective dates. Institutions can retrieve the exact language active at any given time and demonstrate who approved it.

![]()

Safeguard Your Client Relationships

Mitigate Risks with a Modern Customer Communication Compliance Solution

#2. Automating Regulatory Disclosures with Rule-Based Logic

Regulatory exposure often emerges at the point of disclosure selection. Banking communications rarely rely on a single static clause. Disclosure requirements vary by product type, customer profile, jurisdiction, account status, and even transaction history. When selection depends on manual judgment or loosely configured systems, inconsistency becomes likely.

CCM introduces structured logic into that decision layer.

-

Conditional logic engines

Disclosure content is mapped to defined variables such as product category, geography, risk classification, or customer segment. The system determines which clauses must appear based on structured inputs.

-

Metadata-driven content tagging

Regulated language is tagged with jurisdiction, product type, and effective date. The composition engine references these tags during document generation, ensuring accurate inclusion.

-

Automated clause injection

Required disclosures are dynamically inserted into the final document during rendering. Users cannot bypass or remove mandated language without triggering governance controls.

#3. Creating Defensible Audit Trails for Every Communication

Regulatory reviews rarely focus on intention. They focus on evidence. During supervisory examinations, institutions are expected to reconstruct exactly what was communicated, when it was delivered, which version of regulatory language was active, and who approved it. If banks fail to showcase structured traceability, then the responses become fragmented, and credibility weakens.

Here’s how CCM establishes traceability:

-

Time-stamped communication records

Each generated document or notification is logged with generation time, delivery status, channel, and associated customer record.

-

Version history tracking

Templates and disclosure components maintain historical versions with effective dates. Institutions can retrieve the active exact content state at a specific point in time.

-

Retention policy automation

Communication records are archived according to predefined retention schedules aligned with regulatory requirements. Storage policies are enforced systematically rather than manually managed.

What Regulators Expect vs. What CCM Enables

| Regulatory Expectation | CCM-Controlled Outcome |

| Proof of the exact content sent to a customer | Archived copy of the rendered communication with timestamp and version reference |

| Evidence of approval before release | Logged approval workflow with user identity and date |

| Confirmation of which regulatory language was active at the time | Historical template and disclosure version retrieval |

| Demonstration of compliant retention practices | Automated retention enforcement with documented policy rules |

#4. Embedding Data Privacy Controls into Outbound Communications

Data privacy obligations extend directly into customer communication. Regulations such as the General Data Protection Regulation (GDPR) and the Financial Industry Regulatory Authority (FINRA) impose clear requirements for banks around lawful processing, purpose limitation, and controlled use of personal data. When outbound communications are generated without validating consent status or data eligibility, regulatory exposure follows.

In three ways, CCM enforces privacy discipline:

-

Consent validation checks

Before a communication is generated, the system verifies consent status and communication preferences against defined rules. Messages that fall outside permitted parameters are blocked or rerouted for review.

-

Data masking and field control

Sensitive data elements can be restricted, partially masked, or conditionally displayed based on user role, channel, or regulatory requirement. This reduces unnecessary exposure of personal information.

-

Secure transmission alignment

Delivery rules can enforce channel restrictions for sensitive content, ensuring that protected information is transmitted only through approved and compliant channels.

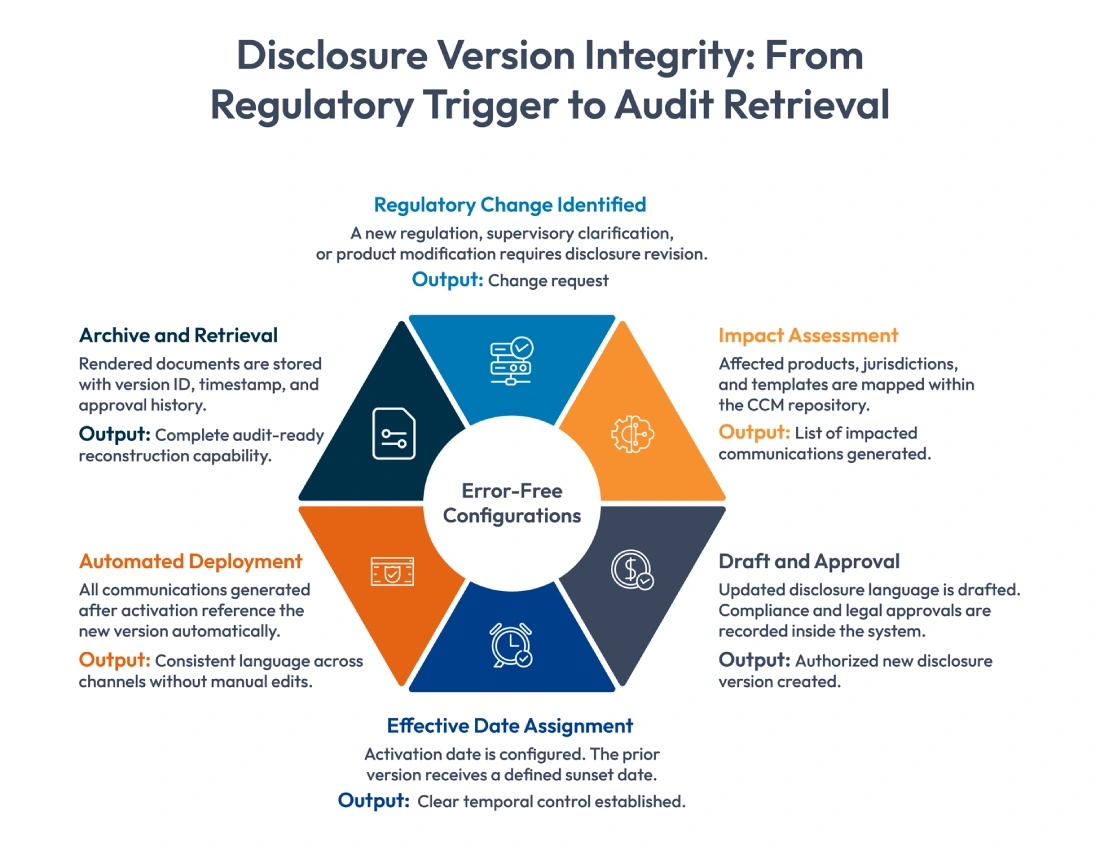

#5. Maintaining Historical Version Integrity of Disclosures

Disputes in banking frequently center on one question: what exactly was communicated at a specific point in time? When product terms evolve, regulatory language is revised, or pricing structures change, institutions must demonstrate which version of a disclosure was active and delivered to a customer on a given date. Ambiguity in version control weakens defensibility.

CCM addresses this through structured version governance.

-

Effective-date versioning

Each disclosure component carries activation and expiration dates. Communications generated during that window automatically reference the correct regulatory language.

-

Archive retrieval capability

Institutions can retrieve the precise rendered document associated with a customer record, including the template version and embedded disclosure state.

-

Regulatory change tracking

Updates to regulated language are logged with documented approval history and impact mapping, creating a traceable record of when and why changes were implemented.

#6. Ensuring Cross-Channel Message Consistency

Regulatory risk increases when the same information appears differently across channels. A rate explanation in a PDF statement must align with the language displayed in the mobile app. A fee disclosure sent by email must match the terms published in the customer portal. Inconsistent wording creates interpretational risk and weakens institutional credibility during supervisory review.

Here’s how CCM maintains consistency

-

Single content repository

Core disclosure components and regulated language are stored centrally and reused across all communication formats.

-

Channel rendering from one source

Email, print, SMS, portal, and mobile outputs are generated from the same structured content objects, with formatting adjusted at the presentation layer rather than rewritten for each channel.

-

Controlled personalization rules

Dynamic customer data is applied through defined logic without altering regulated language blocks.

#7. Monitoring Exceptions and Communication Failures

High-volume communication environments generate operational risk at the point of execution. Notifications may fail to deliver. Messages may be triggered for the wrong segment. Data mismatches can prevent required disclosures from being rendered correctly. When these breakdowns go undetected, regulatory exposure expands quietly.

Customer communication management functions as part of the operational risk framework by introducing structured monitoring and escalation controls.

-

Delivery tracking

Every outbound communication is logged with delivery status, channel confirmation, and failure indicators. Undelivered or bounced messages are flagged automatically.

-

Exception alerts

Rule violations, missing data fields, or incomplete disclosure rendering trigger system alerts before or immediately after generation.

-

Escalation workflows

Defined escalation paths route critical exceptions to compliance or operations teams based on severity thresholds.

-

Integration with risk dashboards

Communication metrics and exception trends can feed into enterprise GRC or operational risk systems, enabling centralized oversight.

Operational Risk View: Without vs. With CCM Monitoring

| Risk Area | Unmonitored Environment | CCM-Monitored Environment |

| Delivery failure | Identified only through customer complaints | Real-time delivery status tracking with automated alerts |

| Incorrect targeting | Detected post-incident during review | Rule validation before dispatch with exception flags |

| Missing disclosure elements | Discovered during an audit or dispute | System-generated alerts at the render stage |

| Escalation handling | Informal email-based coordination | Structured escalation workflows with traceable resolution |

| Risk visibility | Limited cross-channel reporting | Integrated dashboard-level visibility across communication streams |

#8. Enabling Agile Regulatory Change Management

Regulatory change is continuous. Guidance evolves, supervisory interpretations shift, and product rules require adjustment. Delays in updating customer-facing disclosures create measurable compliance lag, particularly in large institutions operating across multiple jurisdictions and channels.

Customer communication management reduces that lag by structuring how changes are implemented.

-

Modular content blocks

Regulated language is managed as reusable components rather than embedded in static templates. Updating a single approved block automatically impacts all dependent communications.

-

Configurable workflows

Regulatory revisions move through predefined approval paths, ensuring compliance validation without informal coordination.

-

Rapid multi-channel rollout

Once activated, updated content propagates across email, print, portal, and mobile outputs without separate manual deployment.

Wrapping Up

These eight capabilities show how customer communication management strengthens regulatory compliance in practical, measurable ways. They reduce ambiguity in what was approved, what was sent, to whom, through which channel, and under which regulatory requirement. That level of clarity is becoming essential.

What is changing is the nature of regulatory scrutiny. Supervisors are increasingly data-driven. Reviews are faster. Sampling is broader. Requests for evidence are more granular. During supervisory examinations, institutions are expected to reconstruct communications at scale, map them to regulatory obligations, and demonstrate control across versions, channels, and customer segments.

That expectation cannot be met through policy documentation or decentralized communication workflows. It requires a structured communication architecture.

CCM becomes the layer that translates compliance intent into executable, trackable, and auditable customer messaging. It creates a linkage between regulatory change, approved language, data usage, distribution logic, and retention. That linkage determines whether a bank can defend its position during an investigation, dispute, or supervisory review.

![]()

Ready to Strengthen Communication Governance?

Schedule a demo to see how Cincom Eloquence can help your team transform customer communications into a controlled, defensible compliance asset.

FAQs

1. How long does it typically take to implement a CCM platform in a banking environment?

Implementation timelines depend on integration complexity, the number of communication templates, and regulatory jurisdictions involved. For mid-sized institutions, phased rollouts can begin within a few months. Large, multi-entity banks often adopt staged deployment aligned with priority risk areas.

2. Does CCM replace existing core banking or document management systems?

No. CCM integrates with core banking, CRM, and document management platforms. It governs the communication layer while leveraging data and workflows from existing systems.

3. Can CCM support multi-jurisdiction compliance requirements simultaneously?

Yes. Advanced CCM platforms allow rule-based content variation, jurisdiction tagging, and region-specific approval workflows to ensure localized compliance without duplicating templates.

4. How does CCM impact customer experience while enforcing compliance?

When properly configured, CCM standardizes regulated language while allowing personalization within approved boundaries. This reduces errors without sacrificing clarity or relevance for the customer.

5. Is CCM relevant only for large banks?

While enterprise banks benefit significantly, mid-sized institutions and credit unions also face regulatory scrutiny. As communication volumes and digital channels expand, structured communication governance becomes increasingly important regardless of size.